Understanding the Mortgage Debt Crisis in Retirement

The dream of home ownership in Australia is rapidly transforming into a nightmare for many Australians approaching retirement age. More and more individuals are choosing to delay retirement because they are still saddled with mortgage debt, leaving them to face a future where their superannuation nest egg may not be enough to cover everyday expenses. In this opinion editorial, we take a closer look at the tangled issues surrounding mortgage debt in retirement, explore the tricky parts of delaying retirement, and discuss possible solutions that can help retirees steer through this challenging period.

Rising Mortgage Pressure and the Shifting Landscape of Home Ownership

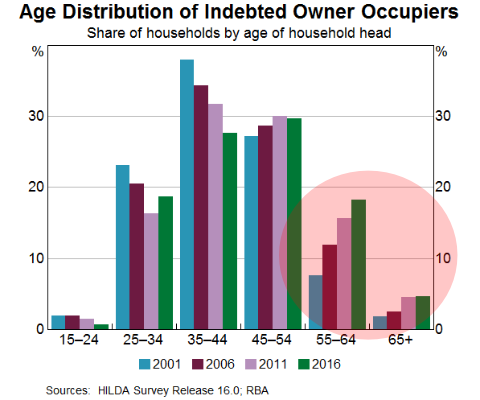

Recent census data reveals that the number of Australians owning their home outright has halved over the past 20 years. At the same time, the proportion of households over the age of 65 still burdened with a mortgage has more than tripled. This dramatic shift is a call for all of us to get into the fine points of how rising housing costs, wage stagnation, and shifting government policies are creating a tough environment for prospective retirees.

Delayed Retirement: A Reality Laden with Hidden Complexities

For many, the increasing mortgage debt is not just a minor inconvenience—it is a full-blown challenge that forces individuals to postpone retirement. The goal to retire at a “normal” age is being pushed back by the ever-growing financial obligations that come with keeping up with mortgage payments, council rates, rent, and other living costs. This reversal in retirement planning is rooted in several subtle parts:

- Escalating home prices that continue to outpace wage growth

- Large mortgage liabilities that can exceed retirement savings

- The additional pressure of refinancing and restructuring debt in later years

These factors combine to create a nerve-racking scenario where retirees find themselves working longer than they had ever planned, all in the hope of managing their lingering financial commitments.

Financial Implications and Everyday Money Stress in Retirement

Mortgage debt in retirement doesn’t only affect the amount of money in the bank; it impacts the quality of life and the ability to enjoy a secure, stress-free retirement. The adverse effects are felt on multiple levels—from the daily worry about meeting payments to the inability to invest in other essential areas, such as health or home improvement.

The Impact on Daily Living and Long-Term Security

The burden of mortgage debt can be overwhelming and leave retirees with less flexibility to manage everyday expenses. Here are a few ways in which this challenge manifests:

- Reduced disposable income: A significant portion of monthly income is dedicated to servicing mortgage debt, leaving less for healthcare, leisure, and unexpected expenses.

- Increased reliance on superannuation: Many retirees are forced to break into their retirement savings to pay off outstanding debts, which contradicts the original purpose of such funds—providing secure retirement income.

- Greater financial stress: The constant pressure to service debt can have a cumulative effect, leading to long-term financial instability and higher levels of stress.

This reality is compounded by the fact that some older Australians find themselves paying thousands of dollars per year in costs such as private health insurance, home insurance, and car insurance. When these expenses are stacked on top of mortgage payments, it creates a full-of-problems situation that further strains their finances.

Housing Market Dynamics: Home Prices, Wage Growth, and Shifting Priorities

The intertwining of home prices and wage growth is central to understanding the mortgage debt crisis. Over recent decades, home price increases have outstripped wage growth, meaning that many Australians are finding it harder to pay for their homes without taking on excessive debt.

Examining the Twists and Turns of the Housing Market

Let’s break down some of the critical elements that are reshaping the housing market and impacting retirees:

- Continuous price inflation: For decades, the rate at which property prices have increased has been significantly higher than corresponding wage growth rates. This mismatch makes it difficult for first-time buyers and established homeowners alike to completely pay off their mortgages by retirement.

- Refinancing and renovation pressures: Many homeowners are forced to borrow against their property for renovations or to support family members entering the housing market, adding even more to their debt burden.

- Transaction and downsizing costs: Even when retirees consider selling their large family homes to downsize, costs such as stamp duty and transaction fees often make the idea less attractive, trapping them in their current situation.

In summary, the housing market is laden with tricky parts and hidden complexities that combine to create a financial environment where managing mortgage debt becomes a major obstacle for those nearing retirement.

Government Policies and the Blame Game: Unintended Consequences

One of the more complicated pieces in this puzzle is the role of government policies, which have sometimes had unintended consequences by exacerbating the mortgage crisis. Several initiatives—such as negative gearing, low interest rate policies, first-time buyer grants, and home builder schemes—were designed to stimulate the housing market and help Australians own homes. However, the long-term impact of these policies is now coming under scrutiny.

Government Initiatives: A Closer Look at Their Long-Term Impact

When we get into the nitty-gritty of government policies, we find a circle of blame that makes it challenging to take decisive action. Here are some of the key policy elements that contribute to the current situation:

| Policy Initiative | Original Intention | Unintended Outcome |

|---|---|---|

| Negative Gearing | Encourage property investment | Increased property prices and investor competition |

| Low Interest Rates | Stimulate economic activity | Large mortgage sizes that accumulate over time |

| First-Time Buyer Grants | Help new buyers enter the market | Boost property demand and further drive up prices |

| Home Builder Schemes | Encourage construction and home ownership | Added pressure on the housing market with limited supply |

These policy initiatives are often intertwined, and the fine shades between their intended benefits and the actual outcomes have left a large portion of the population facing mortgage debt well into retirement. As one industry expert puts it, “Nobody really wants to take responsibility, and this is another classic example where a generation or two of policy choices have led to a rather messy scenario.”

Using Superannuation: A Double-Edged Sword

One response many retirees have had to the growing mortgage debt is to tap into their superannuation funds to help pay down their liabilities. While this approach might provide short-term relief, it also undermines the very purpose of these retirement savings.

Advantages and Pitfalls of Superannuation Withdrawals

There are several considerations for those who decide to use their superannuation to service mortgage debt:

- Immediate relief: Withdrawing part of one’s superannuation can help reduce mortgage debt and preserve home equity in the short term.

- Long-term trade-offs: Reducing superannuation can affect future income streams, leaving individuals with less financial flexibility as they age.

- Cost of alternatives: While some view a reverse mortgage as a viable alternative, these come with high fees and may reduce the inheritance available to heirs.

The choice to use superannuation funds as a debt-payment strategy is not an easy one. The decision is filled with twists and turns and can leave retirees in a more precarious financial position over the long term. It represents a delicate balancing act between providing immediate relief and maintaining long-term financial security.

Downsizing and Retirement Villages: Finding Your Path Through Complicated Pieces

For many Australians burdened with excessive mortgage debt, downsizing represents a super important solution. However, the process of selling a family home and moving into a smaller dwelling is anything but simple. Downsizing involves several steps that require careful planning and consideration of a range of factors.

Challenges and Benefits of Downsizing

While downsizing can be a key element in addressing mortgage debt, there are a few tricky parts to consider:

- Limited suitable housing stock: There is often a shortage of homes that are both affordable and designed to meet the needs of older Australians who wish to age in place.

- High transaction costs: Stamp duties, real estate commissions, and other fees can eat into the equity gained by selling a larger home.

- Emotional attachment: Many retirees are deeply connected to their family homes, making the idea of selling and moving away a nerve-racking prospect.

However, an increasing number of retirement villages and lifestyle communities are emerging as attractive alternatives. These communities often offer facilities and support systems designed to meet the day-to-day needs of older residents—all while costing significantly less than the median house price in the same suburb. For example, a retirement village home can be, on average, 41 percent less expensive than a traditional family home. This difference not only eases the financial burden but also frees up crucial equity that can be redirected toward healthcare or everyday living costs.

Key Strategies for Managing Mortgage Debt in Retirement

In an environment that is full of problems and challenged by tangled issues, finding a clear strategy to manage mortgage debt is essential. There are several approaches that retirees might consider when looking for a stable path forward:

Practical Strategies for Debt Reduction

Below is a list of strategies that can be useful for those looking to reduce mortgage debt before or during retirement:

- Refinance to cut interest rates: In times of economic uncertainty, exploring options to refinance your mortgage can be an effective tactic. This might help to lower the monthly payments and ease the immediate pressure.

- Debt restructuring: Organizing or consolidating debt can sometimes lead to more manageable monthly repayments. Working with financial specialists to sort out a clear plan can help reduce stress.

- Consider reverse mortgages: For those who wish to remain in their homes, reverse mortgages might provide a source of income. However, it is critical to be aware of the high fees and the impact this decision may have on the inheritance you leave behind.

- Downsize strategically: As mentioned, moving to a smaller, more affordable property or a retirement village can provide significant financial relief. Emphasizing properties that are tailored to elderly living can alleviate future health and maintenance concerns.

Table: Comparison of Common Debt Management Approaches

| Strategy | Short-Term Impact | Long-Term Outcome |

|---|---|---|

| Refinance | Lower monthly payments | Reduced interest burden if market conditions improve |

| Debt Restructuring | Simplified repayment plan | Improved clarity on future financial obligations |

| Reverse Mortgage | Immediate cash flow boost | Potentially lower inheritance, high fees |

| Downsizing | Liquidation of excess equity | Long-term financial relief and improved cash flow |

Each of these strategies comes with its own set of advantages and trade-offs, and the best approach will depend on individual circumstances. It is essential to get advice from financial planners who can help figure a path tailored to your specific situation.

The Role of Broader Economic Trends and Personal Preparedness

The rising tide of mortgage debt in retirement is not just a result of isolated financial choices—it is also intertwined with broader economic trends that impact every Australian. When wages remain stagnant and home prices continue to climb unchecked, the scales are tipped in favor of those with significant debt. The clash between these two forces forces many individuals into working longer than they might have planned, ultimately affecting how and when they enjoy retirement.

Understanding the Broader Economic Context

When analyzing the issue, consider these subtle details:

- Inflation and wage stagnation: Rising inflation, combined with little to no real growth in wages, means that even if your income nominally increases over time, it may not be enough to offset the cost of living, especially when balancing mortgage repayments.

- Changing labor market dynamics: With many older Australians remaining in the workforce longer, there is also increased competition for jobs that can accommodate aging bodies and evolving skill sets.

- Social security and government benefits: The age pension and other government supports are often designed with the assumption of a mortgage-free retirement, placing those still paying off debts at a disadvantage.

This combination of factors contributes to a situation where many retirees are forced to extract money from savings meant to fund later life, thereby reducing their overall financial security.

Real-Life Stories and the Emotional Toll

Behind every statistic lies a real-life story of individuals and families struggling with these overwhelming challenges. Many retirees have shared their experiences of having to continue working well into what was supposed to be their retirement years—sometimes driven by necessity rather than choice.

Personal Experiences: The Human Side of Mortgage Debt

The personal impact of carrying a mortgage into retirement is palpable. For instance, one retiree described the constant anxiety of wondering whether they could maintain their standard of living if an unexpected expense arose. Another shared that the decision to use superannuation funds to pay down debt left them with a lingering fear of having insufficient resources for essential healthcare services.

- Stress and anxiety: The mental toll of never truly being free from debt can be exhausting. The pressure of monthly payments, coupled with the fear of not being financially secure enough to handle emergencies, can lead to chronic stress.

- Compromised lifestyle choices: Many retirees have had to cut back on hobbies, travel, and even basic maintenance around the home in order to allocate funds for debt repayments.

- Impact on family dynamics: In some cases, the lack of financial freedom has strained relationships with family, as intergenerational support dynamics shift and children are sometimes expected to step in to help.

These experiences serve as a stark reminder that the issue of mortgage debt in retirement is not merely an abstract economic problem—it is a deeply personal matter that affects daily life and long-term well-being.

Exploring Policy Solutions and Community Initiatives

A comprehensive solution to the mortgage debt crisis in retirement requires not only individual action but also a coordinated response from policymakers. Many experts argue that a multi-level government strategy is necessary to reverse this worrying trend.

Potential Policy Responses and Recommendations

Several key policy changes could alleviate the pressure on future retirees:

- Raising the Age Pension Assets Threshold: Adjusting the assets threshold for the Age Pension may help retirees who are locked into their family homes but have limited liquid assets.

- Smoothing the Transition into Retirement Villages: Easing the roadblocks for retirees who want to “rightsize” into more affordable and suitable housing, such as retirement villages, can provide financial relief.

- Inclusion in the Home Equity Access Scheme: Developing policies that encourage the use of home equity in a secure and controlled manner might offer a lifeline to those struggling with excessive debt.

- Improved Financial Literacy and Planning Resources: Investing in the education of the older population on budgeting, debt management, and retirement planning can help individuals better prepare for these challenges.

In addition to government action, community initiatives and support groups play a role in helping individuals sort out their problematic finances. Organizations like the National Debt Helpline have reported that many contacts from over-60s revolve around issues related to mortgage payments and other living costs. This evidence suggests that combining public policy with grassroots community support may be the most effective way to address the issue.

Strategies for Future Preparedness: Financial Planning and Early Intervention

While addressing the current issues is critical, it is equally important to look ahead and encourage better financial planning among younger Australians. By taking a proactive stance, future generations might avoid many of the tangled issues that their predecessors face in retirement.

Key Recommendations for Financial Planning and Early Debt Management

Here are some actionable steps that both individuals and policymakers can consider:

- Encouraging early financial literacy: Develop workshops and educational campaigns that focus on budgeting, saving, and the risks of accumulating excessive mortgage debt.

- Promoting responsible borrowing practices: Banks and lenders should be encouraged to assess long-term risks more carefully, ensuring that borrowers are well informed of the potential long-term impacts of early debt accumulation.

- Flexible retirement planning: Advisers should help clients build strategies that account for potential delays in retirement, ensuring that individuals are better prepared for the possibility of extended work lives.

- Government support for affordable housing: Policies that aim to increase the supply of affordable family homes could help mitigate the upward pressure on housing prices over time.

These initiatives require cooperative planning between government, financial institutions, and community organizations. The lessons learned from today’s mortgage crisis should serve as a guide to help pave the way for a more secure retirement landscape in the future.

Taking the Wheel: How Retirees Can Manage Their Way Through Debt Challenges

At the personal level, it is essential for those facing mortgage pressure in retirement to remain proactive about managing their finances and preparing for unexpected twists and turns. Although the situation may seem intimidating and even overwhelming, there are practical steps that retirees can take to protect their financial future.

Actionable Steps for Individuals

If you’re dealing with a sizable mortgage as you approach retirement, consider the following small distinctions to help manage the issue:

- Review your budget: Take a close look at your monthly income versus expenses. Identify areas where you can cut back in order to allocate more funds toward debt reduction.

- Consult a financial adviser: Engaging with a professional can help you figure a path that balances your need to maintain your home with the goal of preserving your superannuation savings.

- Explore refinancing options: Even if you are nearing retirement age, there may be refinancing programs available that offer lower interest rates and reduced monthly payments.

- Consider downsizing: Assess whether moving to a smaller, more functional living space might provide financial relief and reduce your ongoing expenses.

Remember, the key is not to panic but to work through the twisted issues one step at a time. While the road ahead may be full of problems, dealing with them in manageable pieces can help alleviate the overall burden.

The Road Ahead: Building a Secure Retirement Despite Mortgage Challenges

Ultimately, the rising mortgage debt in retirement is a nuanced issue that requires both individual determination and collective policy action. While financial hardship might feel overwhelming at times, there are opportunities to reframe the narrative and explore innovative solutions. Retirees and soon-to-be retirees must balance the need to reduce debt with preserving their long-term financial security. The solutions may not be simple, but through a combination of individual adjustment, community support, and policy reform, it is possible to find a path toward a more secure future.

Key Takeaways for a Brighter Financial Future

In summary, here are several essential points that those facing mortgage debt in retirement should keep in mind:

- Plan Early: Establish a realistic retirement timeline and incorporate potential debt repayment strategies well before reaching retirement age.

- Stay Informed: Keep abreast of economic trends, policy changes, and personal finance advice to ensure you are better prepared for emerging challenges.

- Take Action: Whether through refinancing, debt restructuring, or exploring downsizing options, proactive steps can help reduce the financial strain.

- Seek Professional Guidance: Financial advisers and community support organizations can offer tailored advice that considers your unique circumstances.

- Advocate for Policy Change: Engage with local representatives or community groups to support policy changes that can benefit retirees across the nation.

Each of these points is interrelated and represents a piece of the larger puzzle. Managing mortgage debt and planning for retirement are not challenges to be faced in isolation, but rather issues that call for a coordinated, multi-level approach. Addressing them successfully can mean the difference between a stressful, financially constrained retirement and one in which you are free to enjoy the fruits of your lifelong labor.

Conclusion: A Collective Responsibility for a Secure Retirement Future

The rising trend of carrying mortgage debt into retirement is not merely a personal hurdle—it is a societal challenge that calls for a rethinking of both government policies and personal financial strategies. As we have taken a closer look at the issues, from escalating home prices and refund pressures to the consequences of using superannuation as a debt tool, it is clear that a multi-faceted approach is needed.

This op-ed has aimed to dive into the fine points and subtle details of a situation that many now face with a mixture of apprehension and resignation. However, understanding these tangled issues and working through them with practical strategies can empower individuals to figure a path toward financial security. Whether it’s through solid financial planning, considering strategic downsizing, or advocating for thoughtful governmental policy changes, there is hope for alleviating the burden that mortgage debt places on retirement.

While the path is fraught with challenges—from high transaction costs and limited housing stock to the emotional toll of making such significant life changes—every step taken to manage mortgage debt is a step toward a more secure and dignified retirement. With an informed, proactive approach, and a willingness to face the tricky parts head-on, it is possible to steer through these turbulent times. Ultimately, the responsibility lies not only with individuals but with the broader community and government alike. By working together, we can take the wheel and chart a course that ensures our seniors can enjoy the retirement they rightfully deserve.

This discussion is intended to serve as both a call to action and a guide for those currently affected by mortgage debt in retirement. It is a reminder that while the journey ahead may be intimidating and laden with complications, there are clear and practical steps available. With determination, support, and sensible policy changes, the silver tsunami of aging Australians can navigate these troubled financial waters and secure a brighter, debt-managed future.

Originally Post From https://startsat60.com/media/news/the-debt-burden-stalking-aussies-in-retirement

Read more about this topic at

America’s Retirement Crisis Hits a Breaking Point

Addressing the Nation’s Retirement Crisis: The 80%